Before you start house-hunting, calculating your price range is essential.

One of the first steps for those looking to purchase a new home is determining the budget. Many house-hunters do this by examining their monthly income and expenses. You can even use our Mortgage Payment Calculator to estimate your monthly payments. This is a great start, but it’s important to remember that this is only an estimate.

How to Set a Budget for a New House

If you are planning on taking out a mortgage loan to buy a house (which most homebuyers do), the first step is to talk to a loan originator — even before you start house hunting. Why? They will get you pre-approved for a loan, which will tell you the loan amount you qualify for. That amount will be the foundation of your budget.

From there you can work with your loan originator customize your budget based on what you want your monthly payment to be, how much money you’re comfortable putting down, etc.

Another component to consider is your lifestyle and spending habits. One person may love to stay home and work in their garden, while the next wants to eat out frequently and travel internationally. How much of your income is spent on a home will impact ability to do these things after you are a homeowner.

Your loan originator can help you iron out those details and refer you to a local real estate professional who will help you find the home of your dreams. If you're at the start of your homebuying journey, download Your Homebuying Toolkit below to help guide you through the process.

Factors to Qualify for a Mortgage

Mortgages aren’t “one size fits all,” and there are many different mortgage programs to suit each homebuyer’s specific needs. Each loan program has different qualifications and requirements (such as a certain credit score, down payment amount, etc.). However, to qualify for any mortgage loan — and determine the amount you’re qualified for — there are a few key categories lenders look at.

Credit Score

Your credit score is a major factor in the type and size of mortgage loan you will qualify for. To determine this score, the credit bureaus look at a few different factors, such as payment history, types of credit, and more. All these things are good indicators of your likeliness to pay back a loan.

For instance, if your payment history is squeaky clean (you’ve never missed a credit card payment and you always pay the full amount due), it’s safe to assume you’ll have the same habits with your mortgage loan. Your credit score is a reflection of this behavior.

Fortunately, this isn’t the end all be all. If your credit score is less than perfect, there are a variety of mortgage loan programs you can still qualify for. Your loan originator will discuss all your options with you.

Debt-to-Income Ratio

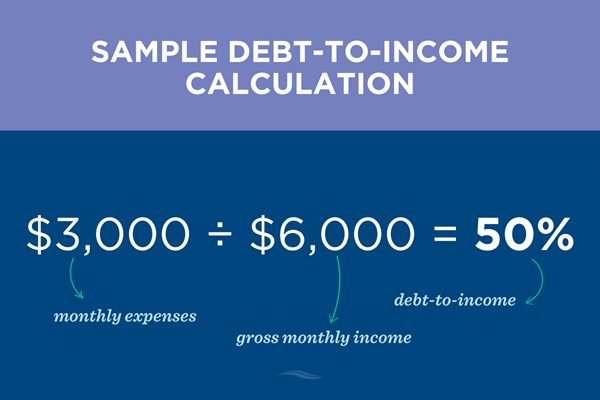

Your debt-to-income ratio (DTI) is just what it sounds like — the amount of debts you owe compared to the amount of income you bring in.

To do a quick calculation of your DTI, simply divide your monthly expenses by your gross monthly income. That percentage is your DTI. When adding up your expenses, only use the following categories:

- Mortgage or rent payment

- Any loan payments (car, credit union, student, etc.)

- Minimum credit card payment

You don’t need to factor in things like grocery, entertainment, or utility expenses.

For example, let’s say these are your monthly expenses in the categories listed above:

- Monthly rent/mortgage payment: $1,800

- Monthly car payment: $700

- Monthly student loan payment: $300

- Monthly credit card minimum payment: $200

This would put you at $3,000 in monthly expenses. If you have a gross monthly income of $6,000, here’s how you would calculate your DTI:

Before a lender can issue you a mortgage loan, it’s important for them to see what other debts you owe. If you are currently tied a high balance of additional loans compared to your income, you might have difficulty paying a mortgage loan. In this example, 50% would be considered a fairly high DTI, and you’d probably need to reduce it before buying a new home.

If your DTI is higher than you’d like it to be, you can lower it by reducing your debt, increasing your income, cutting back on spending, and more. Your loan originator can also provide insight on this.

28/36 Rule

Another unofficial guideline you may want to consider is the 28/36 Rule. While this is more of a “suggestion” than a requirement, it can help you make a smart financial decision concerning your mortgage.

The 28/36 Rule states that you shouldn’t spend any more than 28% of your gross (pre-tax) monthly income on your housing payment (mortgage or rent), and you shouldn’t spend more than 36% of your gross monthly income on all your monthly debt combined (including your housing payment).

Again, this is more of a guideline, but it may help you as you determine your budget for a new home. If your expenses are far above the suggested 28/36 range, you may want to reassess your finances or lower your budget for a new home.

Ready to get started on your journey to your new home? Find a local mortgage expert in your area today.