These terms are often used interchangeably in the mortgage world, but they are three unique processes. Find out which is right for your situation.

Platinum Credit Approval

what is a Platinum Credit Approval?

The Waterstone Mortgage Platinum Credit Approval (PCA) is the strongest mortgage loan pre-approval a homebuyer can receive.

The Platinum Credit Approval process gives you, the homebuyer, the opportunity to submit a full-document loan application before you begin searching for a home. Once the application is submitted, our underwriting team will confirm your eligibility and issue a fully underwritten loan approval — with the exception of the specific property, which you will confirm at a later time. Essentially, you've completed most of the work upfront, so the rest of your loan approval process will be streamlined and simplified!

![]()

With a Platinum Credit Approval in hand, you will have a competitive advantage and the confidence to make a compelling offer on your dream home. In addition, homebuyers with a Platinum Credit Approval experience several unique benefits that make them stand out from other buyers in the market.

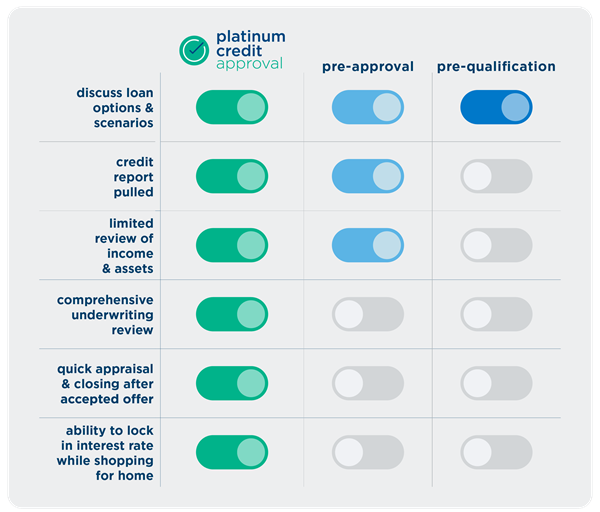

Differences Between Pre-Qualification, Pre-Approval, and Platinum Credit Approval

Benefits to Homebuyers

When you're house shopping with a Platinum Credit Approval, you'll have a variety of advantages over other buyers who are not pre-approved for a mortgage.

Benefits to Real Estate Professionals

Realtors: Your buyers can shop with confidence by securing a full credit approval for their mortgage before beginning the home search process.

Platinum Credit Approval Eligible and Non-Eligible Mortgage Programs

The Platinum Credit Approval Process

As a homebuyer, getting a Platinum Credit Approval could save you time and money throughout the loan process.

FAQs

Platinum Credit Approval is a smart option for buyers. Get a head start on the homebuying process by discovering more about this program!

Photo 1

Photo 2

Photo 3

Differences Between Pre-Qualification, Pre-Approval, and Platinum Credit Approval

Pre-Qualification

Pre-qualification is an informal process where a homebuyer provides their potential lender with some basic information, such as their current income and debt levels. Then, the lender calculates an estimated mortgage loan amount that the homebuyer may qualify for. The key word here is: informal. While a pre-qualification can be helpful at the beginning of your mortgage journey, it’s a very high-level, general estimate. To get a more accurate picture of what you can afford, a pre-approval or a PCA are better options.

Pre-Approval

A pre-approval has a more formalized process than a pre-qualification. If you’re hoping to buy a home and are ready to get pre-approved for a mortgage, we’ll ask you to provide supporting documents such as recent paycheck stubs and bank statements. We’ll also pull and review your credit report. Then, an Automated Underwriting System (AUS), along with our underwriting team, will determine your eligibility. Your Waterstone Mortgage loan originator will review the information in more detail to approve or deny a loan amount.

Platinum Credit Approval

A Platinum Credit Approval (PCA) is the most formal version of the pre-approval process, and it will give you the most accurate picture of the loan amount you may qualify for. To receive a Platinum Credit Approval, you will complete the same steps needed for a traditional pre-approval. In addition, our underwriting team will complete an in-depth analysis of your credit, financial, and employment information. After you make an offer on a property and it’s accepted, you’re well on your way! An appraisal of the property will be completed and — as long as all conditions for the home and the loan are met — a quick closing follows.

Closing Guarantee

We also offer a Platinum Credit Approval Closing Guarantee where, if we are unable to close a Platinum Credit Approval loan — due to an internal error during our underwriting process — we will pay the seller(s) of the subject property $5,000. Learn more.

Photo 1

Photo 2

Photo 3

Benefits to Homebuyers

Photo 1

Photo 2

Photo 3

Benefits to Real Estate Professionals

Experienced Realtors know that a buyer who is ready to make an all-cash offer has a distinct advantage. Homebuyers with cash can close swiftly without last-minute mortgage loan conditions, which is very attractive to home sellers. As a result, real estate agents know that their clients who need financing may find it difficult to compete against all-cash buyers for the same desired property.

Fortunately, a real estate professional whose client has a PCA from Waterstone Mortgage can rest assured that their customer can reasonably compete on a level playing field and realistically win in a bidding war – even against all-cash offers.

Photo 1

Photo 2

Photo 3

Platinum Credit Approval Eligible and Non-Eligible Mortgage Programs

Which mortgage loan programs are eligible for Platinum Credit Approval?

-

Bond and down payment assistance (DPA) programs — ask for details

Which mortgage loan programs are not eligible for Platinum Credit Approval?

-

Brokered loans

-

Construction loans

-

Certain specialty/niche loans

-

Jumbo loans

-

Reverse Mortgages

Photo 1

Photo 2

Photo 3

Platinum Credit Approval Process

The Platinum Credit Approval process is very similar to the pre-approval process, with a few additional steps. If you're interested in obtaining a PCA before you begin home shopping, you can start by completing a loan application (1003) with all the required supporting documents.

Ready to get pre-approved?

Check out this general list of documents you’ll need to gather. Your mortgage loan originator will provide exact details on what is needed, depending on your specific situation and loan type, but it always helps to get a head start!

With your authorization, we will pull a credit report and run the Automated Underwriting System (AUS). Your loan originator and their team will then prepare your loan application package to be submitted to our underwriting team for full review and loan eligibility determination.

Assuming all is in order and your fully documented application is approved by our underwriting team, you will receive a Platinum Credit Approval certificate. At this point, you are now free to shop for your dream home with clarity and confidence!

Finally, all that’s needed is proof of the property’s value (e.g., appraisal) and adequate insurance (e.g., insurance binder). Once these are received, you’ll be well on your way to a speedy closing process.

Photo 1

Photo 2

Photo 3

FAQs

How and where do I apply for the Platinum Credit Approval?

If you have a Waterstone Mortgage loan originator, you can simply ask about getting a Platinum Credit Approval (PCA) before you start home shopping. If not, you can find a WMC loan originator who is local to you. Either way, you can begin the PCA process by completing and submitting your loan application. From there, your loan originator will walk you through the steps of receiving a PCA.

What documents are required for a Platinum Credit Approval?

After you complete and submit your mortgage application, your loan originator will walk you through all the specific documents needed to obtain a PCA. A few of these may include:

- Copy of your driver’s license

- Last 2 years of W2 statements from your employer

- Last 30 days of pay stubs

- Last 2 months of checking account statements — all pages

- Last quarter (3 months) of stocks/bonds/mutual funds/401K — all pages

- Name and phone number of your landlord to verify rental payments, if applicable

- Divorce decree or court order defining alimony or child support payments, if applicable

- College transcripts (if you graduated within the last 2 years)

If you currently own a property, you will also be asked to provide:

- Mortgage statement

- Tax bill

- Homeowners insurance policy

If you are self-employed, you must also provide:

- Last 12-24 months of profit and loss statements

How long does it take to receive a Platinum Credit Approval?

Does a Platinum Credit Approval cost more?

Is a down payment required to qualify for a Platinum Credit Approval?

A down payment is not needed to qualify for a PCA. However, the home loan you decide on may require a down payment — it depends on which type you choose. Your WMC loan originator can walk you through all your options; we have many no-down-payment and low-down-payment loan programs.

How exactly does Lock & Shop work?

Lock & Shop protects homebuyers in markets where interest rates are rising or fluctuating. After you receive your PCA, you’ll lock in your interest rate. You can choose either a 60-day rate lock or a 90-day rate lock.

If you opt for 60 days, you will have 30 days to shop for a home. If you choose the 90-day option, you’ll have 60 days to find a home. The extra 30 days at the end of the rate lock period helps you avoid any extension fees and gives our team time to process things on the back end.

Even if interest rates rise during your rate lock period, your interest rate will remain the same — so you can focus on finding a home you love without rushing to fit a very restrictive timeline.

How long is a Platinum Credit Approval good for?

The timeline for PCA varies, depending on factors such as when your first credit documents were approved and when they expire. Because a PCA varies on a case-by-case basis, it's important to keep in touch with your lender. Your Waterstone Mortgage loan originator can provide an exact expiration date for your PCA, and help you re-apply for a PCA if the need arises.

How does an appraisal work and how is the home's value determined?

A home appraisal is a thorough inspection of the home you’re buying (conducted by a licensed professional) to determine its value. Your Waterstone Mortgage loan originator will order the appraisal after your offer has been accepted by the property’s seller. The appraiser looks primarily at the condition of the home — and the value of comparable properties in that area — to determine the home’s value.

What type of insurance coverage is required?

Homeowners insurance is not required by law; however, it is required by most lenders. Homeowners insurance covers damage to the home, both internal and external. It also covers liability if someone is injured while on your property.

A Platinum Credit Approval is a pre-approval program offered by Waterstone Mortgage. In accordance with federal regulations, consumers are not required to provide verifying documents until they have submitted an application, received a Loan Estimate Disclosure, and stated their intent to proceed with the loan transaction. A pre-approval is not an offer to enter into an agreement, which must be made separately and in writing, and should not be construed as a commitment to lend. Waterstone Mortgage is not obligated to close and fund a loan unless all terms and conditions of the pre-approval have been met. Once a property is selected, Waterstone Mortgage must order and receive a satisfactory flood zone determination, property appraisal, and a satisfactory private mortgage insurance certification, if required. Waterstone Mortgage reserves the right to cancel a pre-approval in the event of any material misrepresentation in the customer's application, in the event of an adverse change in the customer's credit history, employment, income, assets, debt, or other factors affecting their financial status, or if the above requirements are not satisfied.